Phase 1

Understanding and mapping risk

Most financial institutions are exposed to commodity-driven deforestation, conversion, and associated human rights abuse risk through their financing activities. By mapping this exposure, you will be able to effectively identify this risk within your portfolios and take action to address it.

Recommendations for timings to eliminate commodity-driven deforestation, conversion, and associated human rights abuses by 2025:

We recommend that Phase 1 should be started within 3 months of beginning the Roadmap at the latest. We would expect Phase 1 to be completed within 9 months of beginning this Roadmap, or by mid-2022 by financial institutions that adopted the Roadmap at its launch in 2021.

At the end of Phase 1, you will have:

- gained an understanding of deforestation, conversion, and associated human rights abuses and the risks posed to the finance system, your organisation, and your portfolio

- estimated your financial institution’s exposure to deforestation, conversion, and associated human rights abuse risk through its financing activities, and identified opportunities to drive change through your financing activities

- categorised your clients/holdings into high-, medium-, and low-risk based on their exposure to deforestation, conversion, and associated human rights risks

- begun collaborating with other financial institutions and multi-stakeholder groups to address deforestation, conversion and associated human rights risks where appropriate.

Deforestation poses a systemic risk to the finance sector. To eliminate deforestation, conversion, and associated human rights abuses from your portfolio within four years or as soon as possible from starting on this Roadmap, financial institutions should have a clear understanding of deforestation, conversion, and human rights risk in their portfolios in order to be able to manage this risk.

Recommended action 1: Recognise deforestation, conversion, and associated human rights risks

This understanding will provide a solid foundation to build a strong and effective policy on deforestation, conversion, and associated human rights abuse risks for your financing activities.

Understanding these risks will also enable you to align your portfolios with other climate-related policies and targets your organisation has, such as net zero emissions, as well as helping to identify relevant Sustainable Development Goals which might be affected by the environmental and social implications of deforestation including SDG 12 (Responsible Consumption and Production), SDG 13 (Climate Action), and SDG 15 (Life on Land).

Beyond the loss of carbon storage, the loss of biodiversity including through deforestation poses systemic risks, as it reduces pollination, soil fertility, pest control, and resilience to climate shocks. These are foundational processes on which the agricultural system, and the health of the planet, are reliant upon.

If your financial institution is using this Roadmap having never addressed these risks before, there are numerous resources and initiatives which will help to build your understanding of the systemic risk posed by agricultural commodity driven deforestation, conversion, and associated human rights abuses. Some recommended datasets, tools, and guidance pieces are detailed below.

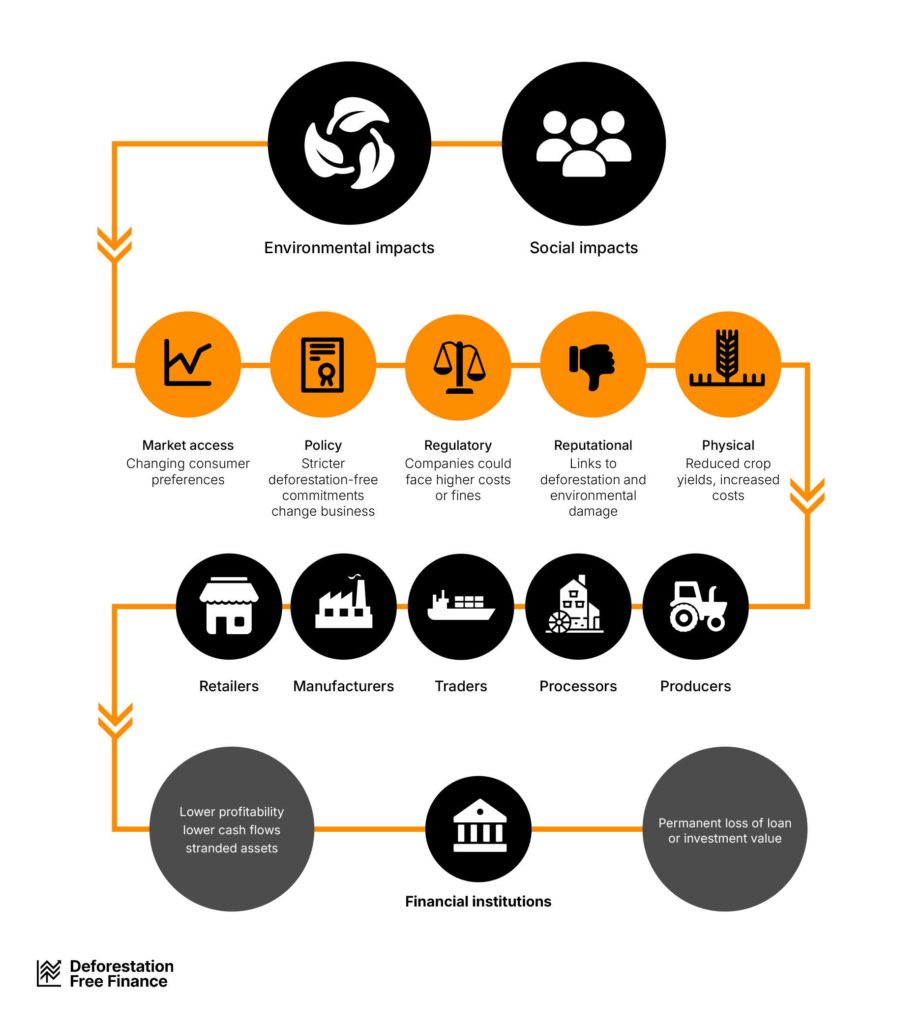

Financial institutions are exposed to deforestation, conversion, and associated human rights abuse risk in multiple different ways. These risks can be in the form of market access, policy, regulatory, reputational, and physical risk, as well as systemic. These are outlined in the graphic below.

The Accountability Framework initiative provides detail on how companies can address their exposure to deforestation, conversion and associated human rights risk through their agricultural commodity supply chains, and is a useful resource to understand how that exposure translates to those financing said companies.

Financial institutions investing directly or indirectly in the Brazilian cattle supply chain are exposed to deforestation, conversion, and associated human rights abuse risk in multiple ways. These risks can be in the form of market access, policy, regulatory, reputational, and physical risk, – as well as systemic, including those outlined in the graphic above. The Brazilian cattle supply chain is uniquely complex, with illegal deforestation and the conversion of natural ecosystems frequently being driven by pastureland, increasing regulatory risks for financiers. This has been a problem across all Brazilian biomes, but 94% of the 50 municipalities with the largest areas of pastureland are located in either the Amazon or the Cerrado. Together, these two biomes account for over 85% of all deforested land in the country in 2023.

Although climate and nature are often addressed separately, it is important to highlight the complex and synergistic interaction between them, driven by strong feedback mechanisms. The Amazon, Cerrado, and other biomes regulate the country’s water cycle, maintain soil fertility, and influence rainfall patterns essential for agricultural productivity. Deforestation disrupts these dynamics, creating cascading effects on different economic sectors, particularly agribusiness.

The supply chain is also closely associated with abuses of labour rights, such as forced labour and modern slavery, the failure to respect the customary rights of Indigenous peoples and local communities to land, resources and territory, and violence toward environmental defenders. Given the increasing global scrutiny of the environmental impacts of Brazilian cattle ranching, the associated reputational risks for financiers are high.

Page 47 of “Navigating deforestation risks and embracing sustainability in Brazilian investments: A guide for investors” by WWF serves as a valuable resource for understanding how deforestation, land conversion, and related human rights risks impact the investors financing these companies. It also explains how Brazilian beef and leather companies can address and manage these risks through their supply chains.

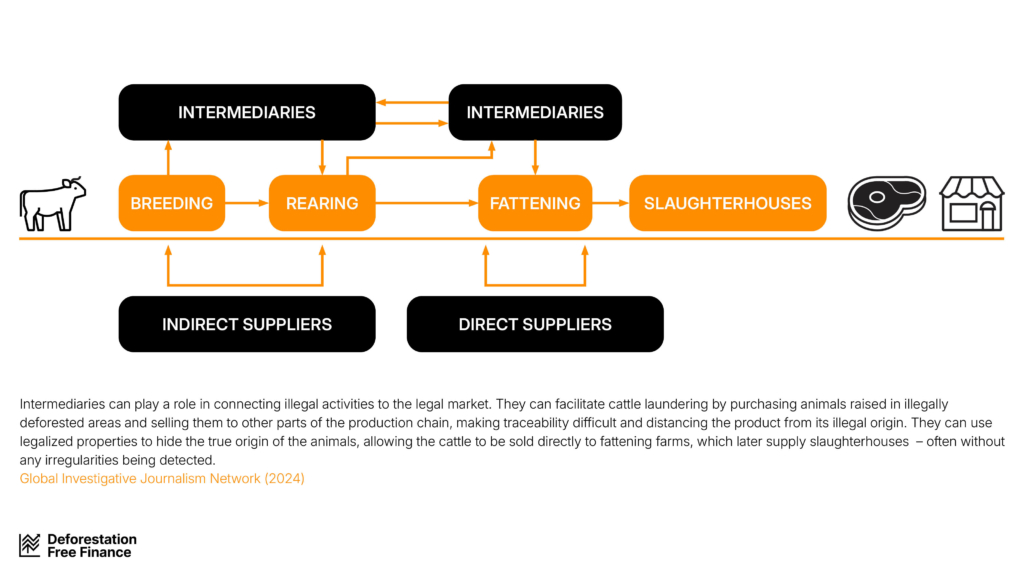

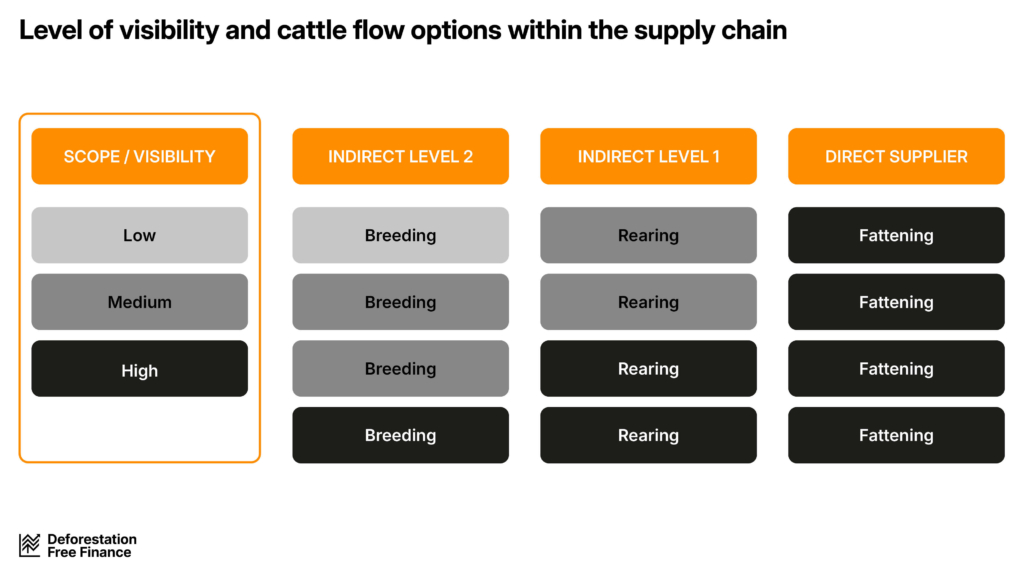

Brazilian cattle supply chains are extremely complex, with multiple actors in even earlier stages of the ‘producer’ supply chain segment. As shown in the diagram below, cattle can move from the birth farm, to a rearing farm, to a fattening farm all before being sent to the slaughterhouse. At each of these stages, there are multiple intermediaries involved, making it difficult to track the true origin of the cattle.

As a result, the risks of deforestation, land conversion, and human rights abuses are not limited to direct suppliers, but can be hidden deep in cattle supply chains through indirect suppliers, leaving companies – and those that finance them – additionally vulnerable to risks.

As cattle products move through these stages of the supply chain, the visibility that companies have of cattle origin decreases. The diagram below shows how much visibility there is of each stage of the farm-stages (breeding, rearing/growing, and fattening), highlighting the complexity of identifying and addressing deforestation, conversion, and associated human rights abuse risks in the Brazilian cattle supply chain.

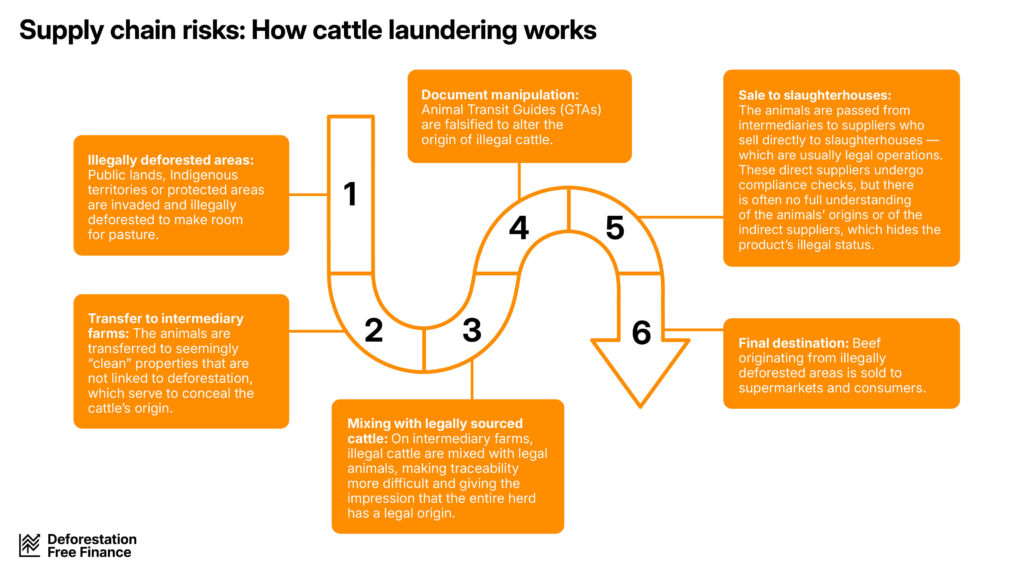

The complexity of cattle supply chains allows illegal deforestation to remain hidden deep within the system. Cattle laundering is a significant challenge in Brazilian cattle supply chains, where ranchers raise their animals in prohibited areas, including illegally deforested or invaded land. To avoid scrutiny, these ranchers often transfer the cattle to legalised lands before sending them to slaughterhouses. This is an important risk for financial institutions to be aware of if they are to ensure that all of their clients/holdings are operating legally. Also, financial institutions can be exposed to money laundering risks by providing financing to companies that are linked to illegal deforestation.

The movement of cattle is regulated by the Animal Transit Guide (GTA), which records information about cattle in batches rather than individually. This limitation facilitates the process of cattle laundering. However, the challenges associated with the GTA go beyond its batch-level recording system. GTA databases are not integrated across states, making it extremely difficult to monitor the movement of animals between jurisdictions. Furthermore, the GTA was designed exclusively for sanitary purposes and does not include critical information about previous properties.

Cross-referencing the GTA with geolocation data from the Rural Environmental Registry (CAR) can enable supply chain companies to achieve a certain level of socio-environmental monitoring of producers’ standalone performance, and is already in use by meatpackers and financial institutions. However, it cannot provide full traceability as it is currently not capable of tracking the full origin of the animal. Financial institutions can support the implementation of more comprehensive traceability mechanisms, and influence clients/holdings to support and participate in such mechanisms.

Financial institutions can also influence clients/holdings to adopt the Beef on Track monitoring criteria which uses Property Productivity Analysis to identify potential signs of cattle laundering associated with circumventing proper documentation of GTA and farm ownership. Without such monitoring criteria and productivity analysis, there is a risk that ranchers could conceal the origin of cattle from deforested areas through avoidance of issuing GTAs at the initial stage. After that, they mix the cattle on farms that meet all legal and regulatory requirements, meaning no environmental violations and no overlap with protected areas or indigenous lands. A GTA is then issued for the batch, creating the appearance that the cattle originated from a legal source. Such laundering schemes can be carried out across multiple farmers, or within a single rancher who owns multiple farms. This strategy allows ranchers to bypass inspections and sell the animals without facing consequences, as the meatpacking system typically only tracks the last farm the animal passed through (direct suppliers), overlooking the earlier farms of the supply chain.

The diagram above details how cattle laundering can work within Brazil, and how risks and impacts of illegal deforestation can be obscured from downstream suppliers, but also from financial institutions. Some practices to improve traceability to tackle cattle laundering include implementing individual identification systems to track cattle from origin to slaughter. Integrating environmental monitoring tools, like satellite imagery from farms, with individual traceability systems provides a comprehensive view of illegal deforestation and conversion risks. Financial institutions can require clients/holdings to adopt practices to improve traceability transparency. Learn more about these recommended requirements in Phase 2.

The following recommendations are useful resources on the risks deforestation poses to the finance sector as a whole, and individual financial institutions. There are plenty of other resources which can provide useful background knowledge on deforestation and the systemic risk it poses.

- ‘Deforestation as a systemic risk’ video from Principles for Responsible Investment provides an overview of how action on deforestation is vital in addressing climate change and achieving net zero commitments, and the risks that deforestation poses to financial institutions and the wider financial system.

- ‘Financing deforestation increasingly risky due to tightening regulatory frameworks’ from Chain Reaction Research highlights how the growing integration of sustainability into financial regulation poses risks to financial institutions exposed to tropical deforestation risk, including compliance, legal, and reputational risks.

- ‘How financial institutions are exposed to deforestation risk’ from Trase provides a useful overview of some of the different ways financial institutions can be exposed to deforestation risk, including through both direct and indirect exposure.

- ‘Investor Expectations On Deforestation In Cattle Supply Chains’ from Principles of Responsible Investment provides a set of expectation for companies which are exposed to deforestation risk through cattle supply chains, including risk management and traceability and metrics and monitoring, but also highlights the key risks – and opportunities – facing companies involved in forest-risk supply chains.

- ‘Investor expectations on deforestation in soybean supply chains’ from Principles of Responsible Investment provides an overview of how companies in soybean supply chains can be exposed to different risks through their operations, particularly in South America, alongside expectations for such companies.

- ‘Investor Expectations on Sustainable Palm Oil’ from Principles for Responsible Investment provides an overview of some of the crucial issues in palm oil supply chains, and provides a set of expectations for companies operating in palm oil supply chains, including to commit to no deforestation, no development on peat, and no exploitation of people and local communities.

- ‘Investor guide to deforestation and climate change’ from Engage the Chain gives useful information on how deforestation is linked to climate risk, as well as the risks that both climate change and deforestation pose to companies in forest-risk supply chains.

- ‘Linking deforestation risks to investment value’ from Global Canopy provides examples of the different kinds of transition and physical risks, alongside real-world examples of these risks in forest-risk commodity supply chains.

- ‘The Collective Effort To End Deforestation A Pathway For Companies To Raise Their Ambition’ from CDP

- Handbook for Nature-related Financial Risks: Key concepts and a framework for identification from Cambridge Institute for Sustainability Leadership

- ‘Forest Governance by Indigenous and Tribal Peoples’ from the Food and Agriculture Organisation of the United Nations provides an overview of how Indigenous people and local communities are critical to forest governance in Latin America.

- ‘Indigenous Peoples And Industrial Corporations’ from United Nations Permanent Forum on Indigenous Issues gives an overview of how corporates can work better with Indigenous peoples

- ‘Assessing The Financial Impact Of The Land Use Transition On The Food And Agriculture Sector’ from Race to Zero looks at how transitioning to a deforestation-free food system will impact companies and financial institutions.

Understand the exposure to transition and physical risks from deforestation, conversion, and associated human rights abuses through Brazilian cattle supply chains

- ‘The Role of Banks and Investors in Deforestation’ from Greenpeace discusses the role of banks and investors in facilitating deforestation in Brazil and possible ways to halt deforestation through financial products.

- ‘Overview of the Beef Chain in Brazil’ from the Indirect Suppliers Working Group provides an overview of the Brazilian cattle supply chain and also explores how different actors along the supply chain contribute to or mitigate the problem.

- ‘Mapping Deforestation Risk of Brazilian Beef Exports’ from Trase maps the deforestation risks associated with Brazilian beef exports, identifying key supply chain actors and their role in driving or reducing environmental impact. It aims to provide transparency for companies and investors seeking to mitigate deforestation risks.

- ‘Transparency in the Cattle Supply Chain in Brazil: Challenges and Opportunities’ from WWF explores the challenges and opportunities in improving transparency within Brazil’s cattle supply chain, highlighting key risks, solutions, and the role of different stakeholders in ensuring sustainable and traceable production.

- ‘Annual Deforestation Report’ from Mapbiomas consolidates data into a document that explores deforestation trends and priority areas for combating deforestation and land conversion year by year.

- ‘Deforestation in the Amazon: Past, Present, and Future’ from Infoamazonia explores the history of deforestation in the Amazon, identifying its causes, current trends, and future risks. It discusses the direct and indirect drivers of deforestation and their impacts on ecosystems and local communities.

- ‘The Cerrado Crisis: Brazil’s Deforestation Frontline’ from Global Witness examines the crisis unfolding in Brazil’s Cerrado region, where deforestation is accelerating. It links agricultural expansion, particularly for soy and cattle, to the destruction of one of the world’s most biodiverse ecosystems, which is under increasing pressure.

- ‘Eye in the Amazon’ from Amazon Watch provides updates for shareholders and activists concerned about rainforest protection and human rights. It focuses on raising awareness of the challenges faced by the Amazon rainforest, emphasizing the importance of preserving biodiversity, supporting local communities, and ensuring the protection of human rights in the region.

- Modefica reports analyze how the fashion industry, particularly leather production, is linked to deforestation risks in Brazil. These reports shed light on the environmental impact of leather sourcing and highlight the role of suppliers in a deforestation-free supply chain.

- Respecting the Rights of Indigenous Peoples and Local Communities from Proforest is a course designed for people working with agricultural supply chains enhancing the understanding of the rights of Indigenous Peoples and Local Communities.

Understand how financial institutions can be exposed to these risks embedded within Brazilian cattle supply chains

- ‘The Role of Traceability Mechanisms in Cattle Production’ from CDP explores the importance of traceability mechanisms in cattle production, linking sustainable practices to forest protection. It highlights how traceability can be a tool for ensuring that cattle production aligns with environmental and deforestation-free standards.

- ‘Indirect Suppliers Monitoring’ from the Indirect Suppliers Working Group provides insights on the tools used and challenges of monitoring indirect suppliers in the beef supply chain. The GTFI shares various tools and approaches that companies are using to track and manage the sustainability of their indirect suppliers, helping to curb deforestation-linked risks.

- ‘Animal Traceability in Brazil: Inputs for a Nationwide System’ explores the establishment of a nationwide traceability system for cattle production in Brazil. It aims to ensure that cattle raised in deforestation-free areas are identifiable and traceable throughout the supply chain, discussing key challenges and solutions for implementation.

- ‘Para State Advanced Program for Cattle Traceability’ focuses on the Para state’s advanced program for cattle traceability. It highlights how this initiative could serve as a model for other states in Brazil, promoting sustainable cattle ranching practices and reducing deforestation, from Nature Conservancy’s Report on Cattle Traceability in Brazil.

- ‘In search of sustainability in the cattle supply chain in the Legal Amazon: what is the role of the financial sector?’ published by Imaflora, provides an overview following the publication of SARB 026/23.

- ‘Beef Transparency in Brazil: Challenges and Opportunities’ published by WWF Brazil in partnership with civil society organizations such as the Brazilian Center for Analysis and Planning (Cebrap), Imaflora, and the Instituto Centro de Vida (ICV), presents a portrait of the cattle ranching supply chain and the main challenges related to transparency.

- The Rural Credit Monitor Panel from Mapbiomas aims to present in a dynamic panel the properties associated with operations registered in the Sicor system that involve public funds. These reports also include cross-referencing with other publicly available databases.

- Traceability in Latin America from Textile Exchange (page 24) explains the meaning and the importance of traceability in Brazil and its panorama to achieve deforestation-free leather supply chains.

Financial Opportunities by Addressing Deforestation

- ‘Financial Opportunities for Brazil from Reducing Deforestation’ from the Environmental Defense Fund examines the potential for green finance to support sustainable development and deforestation reduction, offering a path for investors and businesses to align with environmental goals.

- ‘Mobilizing Capital for Responsible Expansion of Crop & Livestock in Brazil’ from WWF and IFACC focuses on how to mobilize capital to support the responsible expansion of crop and livestock production in Brazil. It explores sustainable agricultural practices that reduce pressure on native ecosystems while meeting rising food demand.

- ‘The Opportunity for Investors in Brazil and Beyond’ from the World Economic Forum outlines the opportunities for investors in Brazil and other regions, emphasizing the role of nature finance in preserving ecosystems while fostering economic growth. It discusses the financial potential of investing in sustainable agriculture and deforestation-free supply chains.

- ‘Expert Discussions on Deforestation and Sustainable Production’ from Tropical Forest Alliance discusses expert views on deforestation and sustainable production, offering insights into how businesses, governments, and investors can collaborate to scale solutions that address both environmental and economic challenges related to deforestation.

- ‘The New Economy of the Amazon’ developed by WRI Brasil in partnership with 76 experts from scientific institutions across the country, demonstrates that preserving the forest is not a threat to development. On the contrary, it presents an opportunity for qualified and inclusive growth in the region.

- Environmental Conduct Guides from TNC aims to establish and standardize criteria for creditors and investors across cattle and soy value chains, enabling them to develop or adapt financial mechanisms for a deforestation and conversion-free (DCF) approach, offering decision-support tools to enhance sustainability in agricultural investments.

- IFACC Market Report brings the progress made in advancing innovative financial products aligned with deforestation- and conversion-free (DCF) products. This report showcases newly launched aligned financial solutions and explores financial structures, disbursement volumes, and the strategies being developed to scale these mechanisms, accelerating the finance transition.

- Investment Requirements from Deforestation-Free Call to Action for Leather Toolkit provides a comprehensive approach of what is expected from the investment side to scale deforestation-free leather.

Recommended action 2: Recognise the business case for acting on deforestation

Risks and opportunities can translate into financial impacts through numerous pathways.

Company revenues and costs can be affected by physical risks such as flooding and changing yields, market risks such as changes in price or availability of inputs such as fertiliser, and regulatory risks such as changes in requirements to develop concessions. Company asset values can be affected by changes in regulations which could make some facilities less viable or result in stranded assets. Cost of capital can also be affected by these risks – potentially increasing the cost of capital for companies that have high exposure to these risks and reducing those costs for companies addressing these risks. Recent green loans and bonds have linked interest rates and coupons to performance on environmental performance.

These risks can impact all financial exposure to a company, including equity and fixed income as they affect a company’s profitability, cash flow or liabilities. Sovereign debt and currencies could also be impacted by risks and opportunities. For example, as markets increasingly become deforestation-free, national economies which have a high dependence on forest-risk commodities will be exposed to market risks that may impact sovereign debt.

Transition risks arise from the capital reallocation decisions associated with the shift to a low-carbon and deforestation-free economy. They include:

- Reputational risks: Brand damage for companies linked to deforestation or unethical practices facing boycotts, public criticism, and reduced consumer trust. This reputational damage can lead to market access risks.

- Market access risks: Changes in consumer and retailer preferences for more sustainably-sourced goods can reduce market access for less sustainably sourced goods, affecting company revenues. These market access risks can be influenced by the broader regulatory and legislative context, detailed below.

- Policy risks: The introduction of more stringent deforestation policies by producers, or their customers (including traders, manufacturers, and retailers), may restrict business practices and strand existing land assets. This is a risk for the producer and their financiers as productivity and extent of land assets is a key element when valuing soft commodity producers.

- Regulatory risks: As governments act to meet their own commitments, including under the Paris Climate Agreement and the UN Sustainable Development Goals, some are introducing legislation to require companies to act on deforestation and other unsustainable practices. The introduction of regulations with conditionalities on exposure of products to deforestation risks can have significant impacts on companies. The introduction of new regulation in demand-side governments, e.g. the EUDR will mean non-compliant companies (as commodities being produced in deforested areas after 31 December 2020) could face financial penalties including fines and seizure of assets. Companies within the jurisdiction of the regulation may also cease to work with suppliers that are non-compliant leading to losses even for those organisations without operations directly within the affected market. Implementation of legislation could impact companies’ access to certain markets or customers, as well as incur financial costs to become compliant with that legislation.

Physical risks arise where deforestation impacts the ecosystem services that businesses depend on. Physical risk can be divided into chronic and acute risks.

- Chronic physical risks refer to the longer-term environmental damages that can occur as a result of deforestation, including increased soil erosion, altered water cycles, disrupted ecosystem services, and potential desertification.

- Acute physical risks refer to more immediate physical dangers that can result from rapid deforestation including flooding, landslides and disruptions to water availability.

Both chronic and acute physical risks can result in financial risk for companies and financial institutions. Clients and holdings linked to soft commodity supply chains rely on the services provided by forests, such as maintaining and regulating regional rainfall, and providing soil stability and wildlife habitat. Through physical risks deforestation compromises these services in both the immediate and longer term, affecting yields, driving higher costs and more volatile commodity prices, with impacts on company cash flow and revenue.

Transition risks arise from the capital reallocation decisions associated with the shift to a low-carbon and deforestation-free economy, and those felt at the global level are also relevant within the Brazilian context. Further examples of transition risks include the exclusion of producers who do not adopt regenerative grazing practices or fail to implement traceability systems that cover indirect suppliers. These risks may arise as companies and markets increasingly shift toward more sustainable production models. They include also:

- Reputational risks: Increased scrutiny on Brazilian cattle supply chains (reference from earlier) may lead to the exposing of unsustainable cattle supply chains. This can lead to market access risks.

- Market access risks: Growing demand from the EU and China for zero deforestation beef, and growing demand for plant-based alternatives can lead to changes in company revenue, and also the exclusion of suppliers that cannot prove sustainable practices or mechanisms to tackle deforestation. This can lead to reduced market access for companies and declining revenues for Brazilian producers and processors/slaughterhouses.

- Regulatory risks: Both national and international legislation impacts Brazilian cattle supply chains, increasing the regulatory risks faced by companies. In Brazil, the Forest Code prohibits the removal of native vegetation from areas after July 22, 2008, and it is estimated that more than 93% of the deforested area in Brazil in 2023 showed at least one sign of irregularity, meaning it either does not spatially match official authorizations or is within protected territories. This indicates that most deforestation occurring in Brazil is illegal, which raises the regulatory risk for many companies.

- New arising regulations, such as Brazilian taxonomy and regulated carbon markets may impose new financing restrictions and emissions limits to cattle supply chains. International regulation, specifically the EUDR, will as of the end of 2025 require proof that beef and leather products placed on or across the EU market to not originate from deforested land, or companies risk fines of 4% of their EU turnover.

Physical risks arise where deforestation impacts the ecosystem services that businesses depend on. Physical risk can be divided into chronic and acute risks.

- Chronic physical risks in Brazilian cattle supply chains pose significant threats to productivity and long-term stability. These risks can lead to lower reproductive rates, slower cattle growth, supply disruptions, and increased price volatility. Key impacts include:

- Loss of forests and biodiversity affects the resilience of ecosystems that support agriculture and pasturelands, such as pollinator populations and organisms present in soil.

- Rising temperatures reduce feed efficiency and increase heat stress in cattle.

- Land degradation can progressively reduce pasture quality. The resultant decline in feed quality directly affects cattle growth, reproductive performance, and overall herd health.

- Reduced water availability can lead to dehydration, heat stress, and increased mortality risk, compromising livestock productivity and resilience.

- Acute physical risks facing Brazilian cattle supply chains can lead to increased livestock mortality and disrupted transportation, as well as reduced cattle health and productivity in the short term. These can be seen through:

- Extreme weather events, including droughts, floods, and storms, which degrade pasture quality and damage infrastructure hindering the transport of cattle.

- Sudden climatic shifts and elevated moisture levels, create favorable conditions for the spread of bovine diseases and parasitic infections.

Both chronic and acute physical disruptions can result in financial risk for companies in cattle supply chains, as shown in the examples above. Through reducing the productivity of agricultural land and increasing direct health risks to cattle, physical risks can reduce productivity and drive higher costs, resulting in negative impacts on company cash flow and revenue.

Financing companies that are committed to deforestation-free production or sourcing can have financial benefits. Companies that produce or source deforestation-free products are not at risk of being held legally responsible or fined for illegal deforestation. This will protect market access, and in some cases may lead to higher price premiums.

Governments are increasingly offering fiscal incentives to companies that adopt sustainable practices, including favorable financing conditions such as lower interest rates or tax benefits. For example, Brazil’s Safra Plan has grown by 26.8% compared to the previous edition, placing greater emphasis on promoting environmentally sustainable production systems. This includes reduced interest rates for pasture recovery and rewards for farmers who implement more sustainable agricultural practices. Investors supporting sustainable livestock farming can capitalize on these opportunities to lower capital costs and enhance project viability. Moreover, green financing options can provide better terms for those investing in sustainable farming technologies and systems, further boosting returns.

Financing companies that are committed to deforestation-free production or sourcing of cattle products can have financial benefits. By promoting sustainable practices in cattle supply chains in Brazil, investors can mitigate climate-related risks and adapt, while supporting agricultural systems that ensure long-term stability and productivity.

With increasing consumer and corporate demand for deforestation-free products, sustainable livestock farming can command a premium in the marketplace. Investing in deforestation-free meat allows investors to tap into this market. As brands and companies strive to meet sustainability goals, they are willing to pay for products that align with their demands, creating new revenue streams for investors.

Green finance in Brazil is evolving quickly. Governments are increasingly offering fiscal incentives to companies that adopt sustainable practices, including favorable financing conditions such as lower interest rates or tax benefits. For example, Safra Plan has grown by 26.8% compared to the previous edition, placing greater emphasis on promoting environmentally sustainable production systems. This includes reduced interest rates for pasture recovery and rewards for farmers who implement more sustainable agricultural practices, in synergy with the National Plan for the Recovery of Degraded Pastures (PNCPD), which targets the recovery of up to 40 million hectares of degraded land. Investors supporting sustainable livestock farming can capitalize on these opportunities to lower capital costs and enhance project viability. Moreover, green financing options can provide better terms for those investing in sustainable farming technologies and systems, further boosting returns.

Another example in this context is that, as the country progresses in the Brazilian Ecological Transformation Plan, the EcoInvest program supports the mobilization of foreign private capital through blended finance instruments, credit lines for project structuring, and mechanisms to hedge foreign exchange volatility. Such initiatives could also present a green finance opportunity for financial institutions.

Deforestation accounts for around 11% of global greenhouse gas emissions, and forests also mitigate climate change by storing carbon, so addressing deforestation is critical to meet net zero targets. Forests are also vital for biodiversity and therefore new commitments to reduce biodiversity loss, such as the Glasgow Declaration on Forests and Land use and the Kunming-Montreal Global Biodiversity Framework, are likely to increase pressure on governments and companies to reduce deforestation.

Climate change is also creating physical risks for commodity production, affecting rainfall, temperatures, risk of floods and droughts, sea level rises and increased pests and diseases. It can lead to reduced productivity, supply chain disruptions, and potentially stranded assets. In turn, these risks can impact returns, liquidity, and the ability to repay loans – undermining asset value and reducing long-term financial stability.

For the financial sector, efforts to combat deforestation can form a key part of meeting emissions targets. In regions where deforestation is a key concern, land use (LUC) changes are major drivers of emissions. In Brazil, deforestation and conversion of natural vegetation for other purposes are responsible for approximately half of greenhouse gas emissions. Therefore, for investors to achieve zero-emission portfolios across these regions and fulfill their climate commitments, it is crucial to address this issue.

Climate change is further intensifying risks to commodity and food production by altering rainfall patterns, increasing temperatures, raising the likelihood of floods and droughts, dropping pollinators population and expanding the spread of pests and diseases. These cascading effects not only threaten food security but also create financial instability across the supply chain.

For example, Investment Funds in Agroindustrial Productive Chains (Fiagro) have faced difficulties as climate-related challenges and rising production costs impact Brazil’s agribusiness sector. Climate risks, combined with financial pressures, have contributed to negative returns in Fiagro funds listed on the stock exchange, with some shares dropping by as much as 12%.

The actions to prioritise as an investor include promoting risk analysis of suppliers in investees, encouraging the adoption of practices that increase productivity on already deforested lands, thus reducing the pressure on new areas, and creating financial mechanisms for ecosystems restoration.

Deforestation and ecosystem conversion is frequently preceded by or occurs in conjunction with human rights abuses, particularly around failure to respect customary rights to land, resources, and territory, communities’ right to Free, Prior, and Informed Consent, and threats and violence towards Indigenous peoples, local communities and Forest, Land and Human Rights defenders. Supply chains and operations associated with deforestation are also frequently linked to labour rights abuses, especially in commodity supply chains.

Without addressing deforestation and conversion, your organisation will continue to be exposed to human rights abuse risks – which may be in contradiction to international human rights legislation and standards, as well as pre-existing policies and commitments.

Deforestation and ecosystem conversion risk in Brazil is deeply connected with associated human rights risks and impacts. Examples include the displacement and marginalization of Indigenous peoples and traditional communities; as forests are cleared for cattle ranching, these communities often face land invasions, forced evictions, and loss of livelihoods. The destruction of forests also undermines their cultural heritage, as these ecosystems are integral to their way of life and spiritual practices.

Deforestation also frequently exacerbates labor rights violations. In areas where illegal logging and unsanctioned land clearance prevail, there are heightened risks of exploitative labor practices, including forced labor and unsafe working conditions. The lack of governance in these regions allows such abuses to persist, often in remote areas where regulatory enforcement is weak. Cattle ranching is one of the sectors to most commonly experience complaints of modern slavery, which cases are on the rise across Brazil.

Escalating deforestation risk and impacts often coincide with threats and violence against forest, land, and human rights defenders . Those who stand up against deforestation and advocate for the protection of rights frequently face intimidation, criminalization, and even assassination. Brazil is among the most dangerous countries for environmental activists.

Without addressing deforestation and conversion, your organisation will continue to be exposed to human rights abuse risks – which may be in contradiction to international human rights legislation and standards, as well as pre-existing policies and commitments. By recognizing the inextricable link between deforestation and human rights, stakeholders can foster more sustainable and equitable practices that safeguard Brazil’s forests and the people who depend on them.

aThe 2021 UK Environment Act introduced due diligence obligations for companies operating in forest risk commodity supply chains, requiring disclosure on steps to identify and mitigate deforestation risks. The introduction of the EUDR in 2023 expanded the geographical scope of companies affected by such disclosure requirements. The EUDR requires companies to develop due diligence systems to identify deforestation exposure for key soft commodities both within and imported into the EU. The scope of due diligence requirements across the EU was expanded through the introduction of the EU Corporate Sustainability Due Diligence Directive (CSDDD) 2024/1760, which introduces obligations for companies to conduct due diligence across a wider range of environmental and associated human rights risks.

These due diligence requirements are further bolstered through enhanced reporting requirements. Legislation on mandatory investor disclosures relating to biodiversity impacts have been enhanced. In 2023, The EU Sustainable Finance Disclosure Regulation, introduced March 2021, was developed through the addition of Principal Adverse Impact Reporting which creates more mandatory requirements for reporting on deforestation risk, biodiversity impact and land degradation. Disclosure Requirements are also a key component of the new EUDR legislation, which requires for companies to disclose conclusive and verifiable information that the products are free of deforestation ranging from geolocational data to disclosures ensuring commodities have been produced in accordance with relevant local legislation.

The EUDR is currently scheduled to come into force on December 30, 2025 for larger companies, and June 30, 2026 for small and micro enterprises. In spite of (proposed) delays to the implementation date, the legislation sets a clear precedent for further legislation globally.

A review of the EUDR is also set to take place in 2025, and will consider the role of financial institutions in preventing financial flows contributing to deforestation and the need for new obligations for financial institutions, creating a direct impetus for financial institutions to address deforestation risks in their portfolios.

The Brazilian Forest Code regulates rural properties and their natural vegetation, requiring landowners to maintain designated areas of native vegetation known as ‘Legal Reserves’ and ‘Permanent Preservation Areas’. However, the Forest Code also allows for legal deforestation within specific limits, as long as the required percentage of the property is set aside for conservation. The required percentage varies by region, with 80% of the property needing to remain forested in the Amazon biome (which can drop to 50% in some circumstances), 35% in the Cerrado within the Legal Amazon, and only 20% in other regions and biomes. These preserved areas are crucial for provisioning ecosystem services, although they are often fragmented and disconnected, which limits the full maximization of these benefits.

The Rural Environmental Registry (CAR) is a key tool for ensuring compliance with the environmental preservation requirements outlined in the Brazilian Forest Code. It facilitates the registration and monitoring of protected areas, strengthens deforestation control, supports environmental regularisation, and enables access to rural credit and incentives. Established in 2012, CAR is a public registry of self-declared environmental information about rural properties in Brazil. All rural properties—including public and private lands, agrarian reform settlements, and areas with traditional communities—are required to register their farm’s boundaries and location in the system. The registry also includes details such as the presence of water bodies, topography, native vegetation coverage, and other environmental factors. CAR has become the most widely used source of information to evaluate socioenvironmental criteria, including those tied to the Public Commitment of Cattle Ranching, a key agreement within the cattle sector.

Some of Brazil’s slaughterhouses and meatpackers are committed to eliminating deforestation in their Amazon supply chains since 2009 through two key agreements the Conduct Adjustment Agreement (TAC) on Meat and the Public Commitment on Cattle Ranching (CPP):

- The TAC (Conduct Adjustment Agreement) is an agreement with the Federal Prosecutor’s Office (MPF) aimed at preventing the purchase of cattle from farms involved in illegal deforestation, embargoed areas, slave labor, or located within Indigenous Lands and Conservation Units in the Legal Amazon. However, inconsistencies in monitoring led to the creation of the Beef on Track (Boi na Linha) Protocol, which initially focused on the Amazon region but was later expanded to the Cerrado as a voluntary protocol. This protocol supports companies trading beef and leather in managing deforestation risks and human rights violations within their supply chains. It also serves as a source of information for financial institutions about the environmental risks associated with their financing. The protocol, which provides guidelines for the socio-environmental monitoring of direct cattle suppliers in the Legal Amazon, has become widely used in financial operations throughout Brazil’s cattle supply chains, including by financial institutions.

- The Public Commitment on Cattle Ranching (CPP) is a voluntary agreement designed to engage meatpackers in eliminating both legal and illegal deforestation from the beef supply chain in the Amazon. It sets criteria for the industrial-scale purchase of cattle and bovine products, aiming to ensure that beef production is free from deforestation, slave labor, and other socio-environmental irregularities.

In 2023, The Self-Regulation System of the Brazilian Federation of Banks (Febraban) launched the Regulation for Managing the Risk of Illegal Deforestation in the Beef Supply Chain, a guideline to monitor credit granted. All the signed financial institutions must follow regulations ensuring their credit operations with slaughterhouses and beef processors do not contribute to illegal deforestation. It means that this regulation can impose credit restrictions on cattle supply chain key actors if they are found to be non-compliant.

This liability of financial institutions in Brazil is also grounded in the provisions of the Brazil Civil Code and the National Environmental Policy (PNMA). Under Brazilian civil code, all parties involved in environmental harm, including financial institutions that fund harmful activities, are collectively responsible for the damage. This aligns with the polluter-pays principle outlined in the PNMA and the precautionary principle in environmental risk management. Financial institutions can be held accountable for the environmental damage caused by their clients, even if they are indirect actors, as affirmed by Brazilian law and upheld by the Superior Court of Justice (STJ). Additionally, financial institutions have the responsibility to respect and avoid infringing upon human rights. They must not only prevent but also remediate any negative impacts they generate, including human rights.

To strengthen efforts to trace cattle back to their origin and assess associated risks—such as deforestation, land conversion, and human rights violations—Brazil’s Ministry of Agriculture and Livestock launched the National Plan for the Individual Identification of Cattle and Buffaloes (PNIB) in 2024. The PNIB aims to implement an individual identification system that records the history, location, and movement of each animal. While its primary purpose is to support animal health programs and ensure compliance with international sanitary standards, the system also holds significant potential as a tool for identifying environmental and social risks linked to cattle production. The plan is divided in phases and envisions full traceability across the national herd by 2032.

Recommended action 3: Collaborate with other organisations

Multi-stakeholder initiatives (those made up of multiple different actors including other financial institutions, companies, NGOs in high-risk countries/regions, and Indigenous peoples and local communities) provide a key opportunity to share knowledge and learn from those addressing deforestation on-the-ground. This is essential in developing and implementing an effective policy on deforestation, conversion, and associated human rights abuses. This can include exchanging knowledge on:

- the drivers of deforestation on the ground

- the critical opportunities and challenges faced by companies, smallholders, and Indigenous peoples and local communities in addressing deforestation on the ground

- why previous efforts to address deforestation have been unsuccessful

- what support from the finance sector is needed.

Continuing this engagement through the following phases and steps of the Roadmap will also serve to strengthen your action on deforestation, and help to further reduce your exposure to deforestation, conversion, and associated human rights risk. This could include:

- biannual meetings with organisations working on deforestation in high-risk regions/countries

- consulting with organisations working on deforestation in high-risk regions/countries in advance of Annual General Meetings (AGMs)

- meetings with associations of Indigenous peoples in high-risk regions/countries.

Many multi-stakeholder initiatives exist to enable rapid progress from financial institutions and companies on deforestation, conversion, and associated human rights abuses risks in Brazil. In addition to the above, this can include exchanging knowledge on:

- the drivers of deforestation on the ground, such as weak land tenure systems and demand for low-cost cattle products in international markets.

- the critical opportunities and challenges faced by producers and ranchers, such as high costs, technological barriers for implementing traceability mechanisms, and limited access to credit for adopting sustainable practices.

- the role of the finance sector, such as promoting access to green financing for cattle ranchers adopting sustainable practices and supporting the development of traceability technologies.

- tracking advancements in cattle sustainability certification, nature-positive projects, and industry progression towards the monitoring of indirect and direct suppliers.

Continuing this engagement through the following phases and steps of the Roadmap will also serve to strengthen your action on deforestation, and help to further reduce your exposure to deforestation, conversion, and associated human rights risk through Brazilian cattle supply chains. This could include:

- Regular consultation with sector associations (like ABIEC, ABRAFRIGO, Brazilian Roundtable on Sustainable Livestock, etc.) and civil society organizations (like IPAM, WWF, ICV, Imaflora, TNC etc.) to align financial strategies with local realities.

- Partnerships with Indigenous associations in regions affected by cattle-driven deforestation, ensuring effective Free, Prior, and Informed Consent (FPIC) processes and respect for customary rights to land, resources and territory.

- Pre-Annual General Meeting discussions with highly exposed companies to promote the sustainable production of cattle products, and ensure transparency on progress towards sustainability commitments.

- Reviewing the progress of ESG-financed projects and their effectiveness in promoting sustainable livestock production.

Investors networks, initiatives and working groups

- Pan-Amazon Network for Bioeconomy promotes sustainable bioeconomy and local leadership in the Amazon, focusing on economic models that prioritize maintaining forests, preserving biodiversity, and ensuring the well-being of local communities.

- The Amazon Investor Coalition unites philanthropists, investors, and corporate buyers with local Amazonian producers, nonprofits, governments, and allies, aiming to increase investments in forest-friendly economies and support conservation finance across the Amazon region.

- PRI Spring is an initiative addressing the systemic risks of biodiversity loss, aiming to protect the long-term interests of investors by contributing to the global goal of halting and reversing biodiversity loss by 2030.

- Innovative Finance for the Amazon, Cerrado, and Chaco (IFACC) aims to significantly increase and accelerate lending and investment in sustainable agriculture across Brazil, Argentina, and Paraguay. IFACC brings together leading companies, banks, and investors to meet the need for transitional finance in the production of beef, soy, and other agricultural products without causing further deforestation or land conversion.

- The Investor Policy Dialogue on Deforestation (IPDD) is a sovereign engagement initiative led by investors that aims to halt deforestation in some of the world’s most biodiverse and carbon-rich biomes.

- The Finance Sector Deforestation Action (FSDA) was launched at COP26 and brings together over 30 financial institutions committed to making their best efforts to eliminate deforestation driven by agricultural and forestry commodities from their investment and lending portfolios.

Cattle supply chain networks and working groups

- Sustainable Cattle Ranching Roundtable is a multi-stakeholder platform that encourages dialogue and action to drive sustainable practices across the Brazilian cattle sector, working towards deforestation-free supply chains.

- Indirect Suppliers Working Group enables companies and investors to understand and address the challenges of monitoring indirect suppliers, managing sustainability, and curbing deforestation-linked risks in the beef supply chain.

- The Leather Working Group is a global multi-stakeholder initiative focused on creating a sustainable leather industry. It aims to ensure that leather is sourced, produced, and used responsibly.

- Leather Call to Action is an initiative to commit to sourcing their bovine leather from deforestation- and conversion-free supply chains by 2030 or earlier. It establishes clear expectations for brands and provides tools and guidance to help them achieve sustainable sourcing practices.

Other approaches

- In Brazil, jurisdictional approaches like the PCI (Produce, Conserve, Include) Strategy in Mato Grosso aim to integrate sustainable livestock production goals with diverse stakeholders, including governments, companies, financial institutions, and producers. These approaches focus on reducing deforestation and promoting sustainable agricultural practices in key regions.

Deforestation-free financial portfolios

Within this roadmap, deforestation-free investments, loans, and portfolios are those that are:

- Deforestation-free

- Conversion-free

- Free from human rights abuse associated with deforestation and conversion

The definitions of each of these terms are detailed below.

Deforestation

This Roadmap uses the definition of deforestation as outlined by the Accountability Framework.

‘Loss of natural forest as a result of:

i) conversion to agriculture or other non-forest land use;

ii) conversion to a tree plantation; or

iii) severe and sustained degradation.’

- ‘Severe degradation (scenario iii in the definition) constitutes deforestation even if the land is not subsequently used for a non-forest land use.

- Loss of natural forest that meets this definition is considered to be deforestation regardless of whether or not it is legal.

- The Accountability Framework’s definition of deforestation signifies “gross deforestation” of natural forest where “gross” is used in the sense of “total; aggregate; without deduction for reforestation or other offset.’

‘Forest’ is as defined by the Accountability Framework initiative.

Conversion

This roadmap uses the definition of conversion as outlined by the Accountability Framework.

‘Change of a natural ecosystem to another land use or profound change in a natural ecosystem’s species composition, structure, or function.

- Deforestation is one form of conversion (conversion of natural forests).

- Conversion includes severe degradation or the introduction of management practices that result in a substantial and sustained change in the ecosystem’s former species composition, structure, or function.

- Change to natural ecosystems that meets this definition is considered to be conversion regardless of whether or not it is legal.’

Human rights associated with deforestation and conversion

This roadmap defines associated human rights as those which are related to deforestation and conversion of natural ecosystems for agricultural and forest-risk commodities. A wide range of human rights are linked to deforestation and conversion, but within this roadmap three specific human rights are included – the right to Free, Prior and Informed Consent, land rights of Indigenous peoples and local communities, and labour rights.

- The right to Free, Prior, and Informed Consent (FPIC) of Indigenous peoples and local communities

- Defined by the Accountability Framework as ‘a collective human right of Indigenous peoples and local communities to give and withhold their consent prior to the commencement of any activity that may affect their rights, land, resources, territories, livelihoods, and food security. It is a right exercised through representatives of their own choosing and in a manner consistent with their own customs, values, and norms.’

- The customary rights of Indigenous peoples and local communities to land, resources, and territory

- Defined by the Accountability Framework as ‘patterns of long-standing land and resource usage in accordance with Indigenous peoples’ and local communities’ customary laws, values, customs, and traditions.

- Such rights apply to the lands, resources, and territories that Indigenous peoples and local communities have traditionally owned, occupied, or otherwise used. They do not apply to lands, territories, and resources that these groups have acquired in other ways, such as by purchase or part of a compensation package.

- These rights are a collective human right of Indigenous peoples and local communities that exists whether or not a title from the State has been issued.’

- Zero tolerance for threats and attacks against environmental and human rights defenders

- In line with the standards outlined by the Zero Tolerance Initiative.

- Labour rights of workers (including contractors, smallholders, and temporary staff) at the points of production, including from the point of forest clearance to active production, for the highest forest-risk commodities. Where a financial institution or company is engaging with or monitoring a supply chain for deforestation or land rights risks, labour rights should be included in engagement or monitoring efforts in order to eliminate abuses of these rights too

- As defined by the Accountability Framework Core Principle 2.3 this includes the right to have freedom of association, and to be free from forced labour, child labour, and discrimination in line with the ILO, and to ensure no abusive practices or undue disciplinary procedures, legal and decent working hours, safe and healthy workplaces and living wages and fair benefits.

Nature- and people- positive

Nature-positivity is halting and reversing nature loss. Naturepositive.org highlights three key steps to achieve nature-positivity including zero-net loss of nature from the end of 2020, net nature-positive by 2030, and a full recovery of nature by 2050.

Nature- and people- positive financing is finance that makes progress towards halting and reversing nature loss while respecting and protecting the rights of humans who are dependent on or inhabit the land in question.

Deforestation and Conversion-Free Commitment

‘A public statement by a company/financial institution that specifies the actions that it intends to take or the goals, criteria, or targets that it intends to meet with regard to its management of or performance on environmental, social, and/or governance topics.

Commitments may also be titled or referred to as policies, pledges, or other terms.’

‘Commitments may be company-wide (eg, a company-wide forest policy) or specific to certain commodities, regions, or business units. They may be topic specific or they may address multiple environmental, social, and/or governance topics.’ See more at the Accountability Framework definition.

Implementation Plan

A documentation of the activities an organisation plans to carry out to address environmental or social issues or to fulfill commitments, policies, goals, or other obligations and can be a useful guide for each step planned to a deforestation-free portfolio.

Supplier engagement plan

‘Documentation of the actions that a buyer intends to implement to support its suppliers and help ensure that these suppliers comply with the buyer’s social and environmental commitments, policies, goals, targets, and other obligations.’ See more at the Accountability Framework definition.

An Accountability Framework aligned engagement plan can help companies understand how to engage suppliers (or for financial institutions to engage with clients/holdings) and track their progress in line with the Accountability Framework. Engagement plans are important to keep track of non-compliant suppliers’ progress to reinsert them into the supply chain.

Some examples:

- Identify high-priority suppliers: Identify suppliers that present the highest level of non-compliance

- Save time and cost: Integrate manual supplier assessment questionnaires into one platform

- Plan field visits: Plan field visits or investments in improving practices

Cutoff date

A cut-off date is the date after which deforestation or conversion renders an area or production unit non-compliant with no-deforestation or no-conversion goals, commitments, targets, or other obligations. For instance, a cut-off date of 2020 means that companies or producers sourcing from land deforested or converted after 2020 will not receive financing or market access.

Target Date

A target date means the date by which an organisation aims to have fully implemented its commitment or policy. For example, a target date of 2025 indicates that by that year, the financial institution commits to having fully met its commitment.

Traceability

Traceability is defined as the ability to follow a product or its components through the stages of the supply chain (e.g., production, processing, manufacturing, and distribution). Full traceability systems should be able to track the origin of the commodity and it is often interpreted as the ability to verify the history, location, or application of an item through documented and recorded identification.

Compliance/Non-compliance

The state of complying (compliant) or not complying (non-compliant) with or fulfilling a given commitment, policy, other obligation.

In the context of the Accountability Framework, non-fulfilment of voluntary commitments and policies, non-compliance with applicable law, and adverse impacts to internationally recognised human rights are all considered instances of non-compliance.

Disclosure

Disclosure is the public sharing of information by companies. This can include reporting that is available to the public as well as free public sharing of other information, such as company policies and commitments; company business structures, affiliates, and financial interests; supplier lists; conflicts of interest; or political action (lobbying, campaign contributions, etc). Disclosure is a mechanism for transparency.

Due diligence

Due diligence is a risk management process implemented by a company to identify, prevent, mitigate, and account for how it addresses environmental and social risks and impacts in its operations, supply chains, and investments.

Legal Amazon

The Legal Amazon (“Amazônia Legal”) is a defined administrative region in Brazil that covers approximately 59% of the country’s territory. It includes nine states: Acre, Amapá, Amazonas, Maranhão (partially), Mato Grosso (partially), Pará, Rondônia, Roraima, and Tocantins. This region was established to promote social and economic development while considering the unique environmental characteristics of the Amazon. Although it overlaps significantly with the Amazon Biome, the Legal Amazon also includes areas of the Cerrado and Pantanal, making it broader than the strictly ecological definition of the Amazon. It’s often the focus of conservation policies, deforestation monitoring, and sustainable development programs.

Cattle direct and indirect suppliers

- Direct suppliers: These are ranches that sell cattle directly to meatpackers or slaughterhouses, often involved in the final stage of the cattle rearing process. . These suppliers can typically provide more traceable information about the cattle they sell since their transaction is straightforward and directly linked to the processing stage.

- Indirect suppliers: These ranches or intermediaries do not sell directly to the meatpackers but instead sell or transfer cattle to other ranches or traders. This category often includes auction houses, middlemen, smallholders and traders who move cattle between various ranches or regions before they reach the slaughterhouses. Since cattle can change hands multiple times, tracking their journey becomes more complicated, posing challenges for maintaining accurate traceability and monitoring.

GTA – Animal Transit Guide

The Animal Transit Guide (GTA) is an official document required in Brazil to track the movement of livestock, ensuring their traceability, health status, and compliance with sanitary regulations. It includes key information such as the origin, destination, and identification of the animals, along with details about any health checks or vaccinations. The GTA aims to prevent the spread of diseases, ensure proper animal welfare, and monitor the legal and ethical movement of cattle. However, it can be compromised through practices like cattle laundering, where falsified,manipulated or omitted information can conceal the true origin of the animals.

CAR – National Environmental Registry

The Cadastro Ambiental Rural (CAR) is a national environmental registry in Brazil designed to monitor and manage the use of rural properties. It requires landowners to register their properties and provide information about their environmental preservation areas, such as forests, riparian zones, and protected habitats. The CAR aims to promote sustainable land management, ensuring compliance with environmental laws, especially those related to deforestation, and supports efforts to restore degraded lands. By creating a digital record, it helps authorities track land use and improve environmental monitoring. The CAR is self-declaratory, meaning landowners provide the information themselves.

Cattle laundering

Cattle laundering refers to the illegal practice of disguising the origin of cattle, often to bypass regulations or to hide the involvement of cattle in illegal activities, such as deforestation, land grabbing, or the use of cattle for illicit purposes (e.g., in illegal slaughterhouses).

Conducting an initial assessment of your financial institution’s exposure to deforestation, conversion, and associated human rights risk will enable you to understand your overall risk profile and identify the highest-risk customers/clients in your portfolio which you can prioritise for more in-depth risk assessment (see Phase 2) and engagement. It will also provide you with a baseline of exposure – which you can report progress against – and preliminary information to inform the development of your policy in Phase 2.

Recommended action 1: Identify profile of clients/holdings with likely high exposure to deforestation risk

Some sectors and industries have a greater exposure than others to deforestation, conversion, and associated human rights risks, and you can use the data sources highlighted below to identify which clients/holdings are likely to have high exposure to deforestation, conversion, and associated human rights abuse risks. This information will allow you to identify priorities for in-depth risk assessments and engagement in later Phases.

This action has two key steps: to identify whether the client/holding is in a high-risk sector, and to identify whether they have been categorised as a high-risk client/holding by any third party data providers. Additional guidance on data sources for this step are included below.

A full list of high-risk sectors linked to deforestation can be found in the appendices using GICS categorisations which can be used to identify which of your clients/holdings are potentially exposed to high deforestation, conversion, or associated human rights abuse risks.

There are also datasets and tools which you can use to determine whether any of your clients/holdings have already been identified as high-risk by third party data providers. This can include Forest 500, CDP Forests, ZSL SPOTT, Global Forest Watch Pro, Forests & Finance, and Trase. A more comprehensive list of tools, including descriptions of how they can best be used for high-level risk assessments, can be found below.

This information will be built on in the in-depth risk assessment in Phase 2 Step A.

Some companies have a greater exposure than others to deforestation, conversion, and associated human rights risks, and you can use the data sources highlighted below to identify which clients/holdings are likely to have high exposure to deforestation, conversion, and associated human rights abuse risks through their direct or indirect involvement in Brazilian cattle supply chains. This information will allow you to identify priorities for in-depth risk assessments and engagement in later Phases.

This action has two key steps: to identify whether the client/holding is linked to a high-risk region, and to identify whether they have been categorised as a high-risk client/holding by any third party data providers. Additional guidance on data sources for this step are included below.

Firstly, for producers and processors prioritize assessments of properties or suppliers operating in regions with high deforestation rates (e.g., municipalities included in the SEEG list of cities as high greenhouse gas emitters in land use in recent years, or consult the list of municipalities prioritized by the Ministry of the Environment). For meatpacking companies, it is recommended that financial institutions collaborate closely with these businesses to gain a comprehensive understanding where the facilities and suppliers are located. A key focus should be on the number of suppliers and volume sourced from them in sensitive areas like the Amazon and Cerrado biomes, areas at high risk for deforestation, land conversion, or human rights abuses.

There are also datasets and tools which you can use to determine whether any of your clients/holdings have already been identified as high-risk by third party data providers. This can include Trase (focused on soy and beef supply chains), Global Forest Watch Pro (identification of deforestation hotspots), Forest IQ (which brings together aligned, best-in-class, and actionable data on how more than 2,000 major companies are addressing their links to deforestation), CDP (scores can be consulted for a general understanding of companies), reports from Observatório do Clima, meatpacking audit results published by Amigos da Terra – Amazônia Brasileira, and the Floresta 250. A more comprehensive list of tools, including descriptions of how they can best be used for high-level risk assessments, can be found below.

This information will be built on in the in-depth risk assessment in Phase 2 Step A.

- Ceres’ ‘Investor Guide to Deforestation and Climate Change’ provides detailed guidance on how to assess your deforestation risk including the identification of high-risk countries/regions, with a particular focus on how this can be linked to engagement activities.

- ‘Deforestation tools assessment and gap analysis: How investors can manage deforestation risk’ from the WBCSD provides guidance on key frameworks and 14 tools to implement deforestation free finance, indicating which tools and datasets are relevant for specific use cases for investors and banks.

- WWF’s ‘Assessing portfolio impacts’ provides guidance on how different tools can be used to assess biodiversity and SDG footprints, with a focus on impact assessments.

- For supplementary tools and datasets specific to Brazil, refer to Phase 2.

Country-level data

- UN COMTRADE provides data on the trade value and volume of commodities, and all associated derivatives, from all countries

- MapBiomas provides historical data on the land use cover in Brazil, allowing greater visibility of which areas/regions are most at risk of deforestation

- Verite Commodities Atlas provides country level data on the risk of child and forced labour in commodity supply chains

- IBAT (Integrated Biodiversity Assessment Tool) holds three key datasets – IUCN Red list of Threatened Species (the STAR layer is of particular relevance to this Guide), the World Database on Protected Areas, and the World Database of Key Biodiversity Areas. This can be used to identify high-risk regions

Company risk exposure and performance profiles

- Business & Human Rights Resource Centre stores news and allegations relating to the human rights impacts of over 20,000 companies. Depending on the availability of data, this ranges from a handful of articles to over a decade of news stories, civil society reports and company disclosure.

- CDP Forests assesses companies on their progress towards removing commodity-driven deforestation and forest degradation from their operations and supply chains, based on their CDP disclosures

- ENCORE maps the impacts and dependencies of economic sectors on nature, and can be used to identify and assess nature-related risks at a sector and sub-sector level

- Global Canopy’s Forest 500 and Forest 500 – Finance projects identify the 500 companies and 150 financial institutions with the greatest exposure to tropical deforestation risk through their production, processing, procurement, and financing of the nine highest-risk forest commodities. The open-access dataset also includes data on volumes of commodities used, as well as a total score for each company and financial institution for their performance on deforestation and associated human rights abuses.

- Global Canopy’s Floresta 250 project identifies the 175 companies and 75 financial institutions with the greatest exposure through their production, processing, procurement, and financing of beef and leather products.

- Forest IQ brings together aligned, best-in-class and actionable data how more than 2,000 major companies are addressing their links to deforestation using three core metrics, namely: exposure, materiality and performance on reporting. It provides open data and metrics, alongside a tailored offering for financial institutions to help enable their transition to deforestation-free financial portfolios.

- Forests and Finance assesses the financing of 300 companies in forest-risk commodity supply chains, and evaluates the policies of financial institutions involved

- Global Forest Watch Pro uses geospatial data to monitor companies and banks in forest-risk commodity supply chains, and can be used to understand the extent of deforestation in forest-risk commodity supply chains and financing

- Trase maps forest-risk supply chains linking consumer countries, and traders with places of production, allowing banks and investors to see which of their holdings are exposed to potentially high-risk regions and commodities.

- ZSL SPOTT assesses palm oil, timber, paper and rubber producers and processors on the strength of their ESG policies

Geospatial data

- Nusantara Atlas provides maps of concessions and mills for wood pulp and palm oil in South East Asia

- Global Forest Watch Pro uses geospatial data to monitor companies and banks in forest-risk commodity supply chains, and can be used to understand the extent of deforestation in forest-risk commodity supply chains and financing

- Land Matrix provides information on large agricultural investments and land acquisitions in almost 100 countries, including information on investors, commodity, and scope

- Environmental Justice Atlas maps socio-environmental conflicts, and can be used to understand key socio-environmental risks related to forest-risk commodity production in specific regions

Human rights risk data

- UN Human Rights Treaty Body database provides details of records and observations from different Human Rights Treaty bodies, which can be filtered by country and Human Rights Treaty body

- Land Portal Geoportal provides a map with layers on forest tenure, corruption, forest landscape restoration, and Indigenous and community land rights

- Landmark map of indigenous and community lands, which can be used to identify where Indigenous peoples hold rights to land, resources, and territory and which regions may be at risk of conflict over land use rights and Free, Prior, and Informed Consent

- Verite Commodities Atlas provides country level data on the risk of child and forced labour in commodity supply chains

- Environmental Justice Atlas maps socio-environmental conflicts, and can be used to understand key socio-environmental risks related to forest-risk commodity production in specific regions

Note that although these datasets and tools are helpful in understanding deforestation, conversion, and associated human rights risks, none provide all of the relevant data and information on their own. They are best used in combination with each other. A further list of applicable datasets and tools is available from the Accountability Framework initiative.

As defined by the Forest 500 selection methodology. The Forest 500 does not cover all possible commodities, and for some countries other commodities will be more important.

| Country | Key forest-risk commodities produced |

| Argentina | Soy, Cattle, Timber |

| Australia | Cattle, Timber |

| Bolivia | Soy, Cattle |

| Brazil | Palm, Soy, Cattle, Timber, Cocoa, Coffee, Rubber |

| Cambodia | Rubber |

| Cameroon | Palm, Cocoa |

| Canada | Soy, Cattle, Timber |

| Central African Republic | Coffee |

| China | Soy, Cattle, Timber, Rubber |